Manually entering income and expenses into a spreadsheet to create a profit & loss report is time-consuming and prone to errors. If you miss one comma or mistakenly edit a formula, you’ll mess up your entire accounting report.

There’s a more efficient way to do short-term rental accounting. Accounting software connects directly to your bank accounts and automatically generates entries for each transaction. Most accounting platforms integrate with your property management software (PMS) and handle revenue, receipts, and payment information for multiple properties.

By the end of this article, you’ll be able to know when to use vacation rental accounting software, which one to choose for your business, and how to do trust accounting.

When should you use accounting software for vacation rentals?

If you manage one or two short-term rental properties, you can probably keep track of your transactions on a spreadsheet. However, you might need accounting software if:

Your business is growing

Manually entering daily transaction data isn’t an efficient process. And as you grow, you need to find ways to streamline and automate as many tasks as possible. If you find yourself spending more time on bookkeeping, it might be time for you to find and pay for an accounting tool to properly manage vacation rentals.

You need faster access to insights

Since manual bookkeeping is a cumbersome process, you may not have the data available when you need to make decisions. That can lead you to follow your gut or delay important choices. If this is happening to you, it’s time for you to think about using accounting software.

You’re making mistakes

Bookkeeping is a way of accurately recording your business’ transactions one by one. Making mistakes can jeopardize your business finances and cash flow. If you’re spotting mistakes in your reports, you should look into accounting software.

The 6 best vacation rental accounting software tools

Finding the right accounting software for your short-term rental isn’t an easy task. That’s why we’ve compiled a list of six bookkeeping software, including its pros, cons, pricing, and best features to simplify the selection process. These are:

- Clearing

- Ximplifi

- Quickbooks Online

- Xero

- Sage Intacct

- FreshBooks

1. Clearing

Clearing is more than just a financial management tool—it’s an all-in-one financial operating system tailored specifically for Short-Term Rental property managers. Clearing’s platform integrates seamlessly with Hostfully, OTAs, and financial institutions, transforming complex data into actionable insights and comprehensive financial reports that keep you in control.

Key features and benefits

- Automated Bookkeeping: Clearing matches booking information and bank account deposits automatically, closing your books faster than ever.

- Trust Accounting: Segregate funds by homeowner or group of properties.

- Payments: Move funds with Clearing’s ACH payment system to simplify vendor and owner payments.

- Bank Account Reconciliation: Reconcile any bank account connected to Clearing, or opened through Clearing, all in one place.

- Financial Reporting: Clearing provides comprehensive reporting, including: homeowner, management, profit & loss statements, cash flow, and tax reports.

- Expense Management: Categorize, split, and allocate expenses by homeowner and/or property.

Pricing

Pricing for Clearing is available here: https://www.getclearing.co/pricing

Pros

- Clearing provides comprehensive financial oversight, allowing you to manage all aspects of your short-term rental business’s Trust Accounting from one intuitive platform, which streamlines operations and reduces costs.

- Clearing scales to meet your growing business needs.

- The platform is designed with user-friendliness in mind, enabling you to quickly access vital information.

- Provides dedicated support to guide you through any challenges, ensuring you maximize the software’s benefits.

- You can leverage the expertise of leading accounting firms in the short-term rental industry with Clearing, training your existing accountant or bookkeeper, or opting for one of Clearing’s preferred partners for a seamless experience.

Cons

- Clearing’s main market is multi-property managers, though smaller property managers can still gain value from the software’s tools.

- Core focus is on Trust Accounting.

- While Clearing can be beneficial for owner-operators to reduce the time they spend bookkeeping, some businesses may want to utilize the Quickbooks integration for further corporate capabilities.

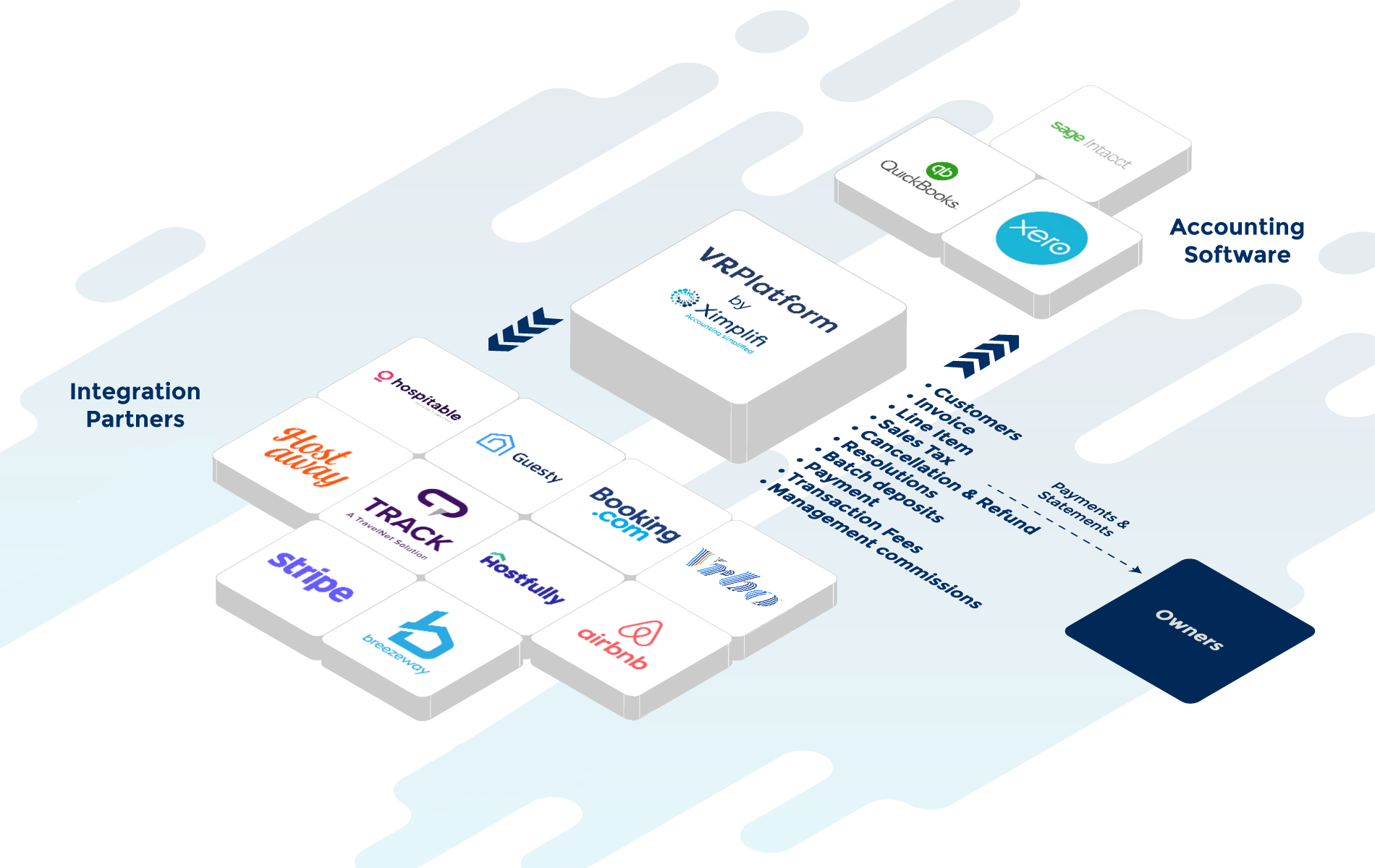

2. Ximplifi

Source: Ximplifi.com

Ximplifi isn’t so much an accounting tool as a full-service accounting company that offers advisory and consulting services, accounting services, and technology solutions. That means, they’ll help you:

- Identify your accounting needs

- Manage the integration of their tools with your PMS

- Handle all accounting transactions

- Share automated reports

Key features and benefits

- Holistic accounting support: Ximplifi offers these three products to better serve your needs

- VRAccounting: uses outsourced accounting tools to handle your day-to-day accounting tasks.

- VRPlatform: removes manual data entry and gives you the most updated accounting data.

- VRConsult: analyzes your needs and sets up software for you.

- Integrations: Ximplifi integrates with different PMS like Hostfully, Hostaway, Guesty, Track, and Hospitable.

- Accounting software: this company uses top-notch accounting software to operate (QuickBooks, Sage Intact, and Xero).

Pricing

Pricing for Ximplifi is only available through a personalized quote.

Pros

- It works with accountants that handle your income and expenses for a fraction of the price of hiring full-time professionals.

- If you have a staff, Ximplifi runs payroll for you and pays service bills on time.

- Ximplifi syncs guest invoices upon confirmation or cancellations for accurate bookkeeping.

- This company registers deposits, Stripe, and does Airbnb payment processing daily.

- Ximplifi integrates with Hostfully and other PMS.

Cons

- It’s not software so it might be more expensive than paying for a typical license.

- Ximplifi has a team of real accountants, which means you’ll need to get to know them and adjust to their style. However, Ximplifi users are satisfied with their work.

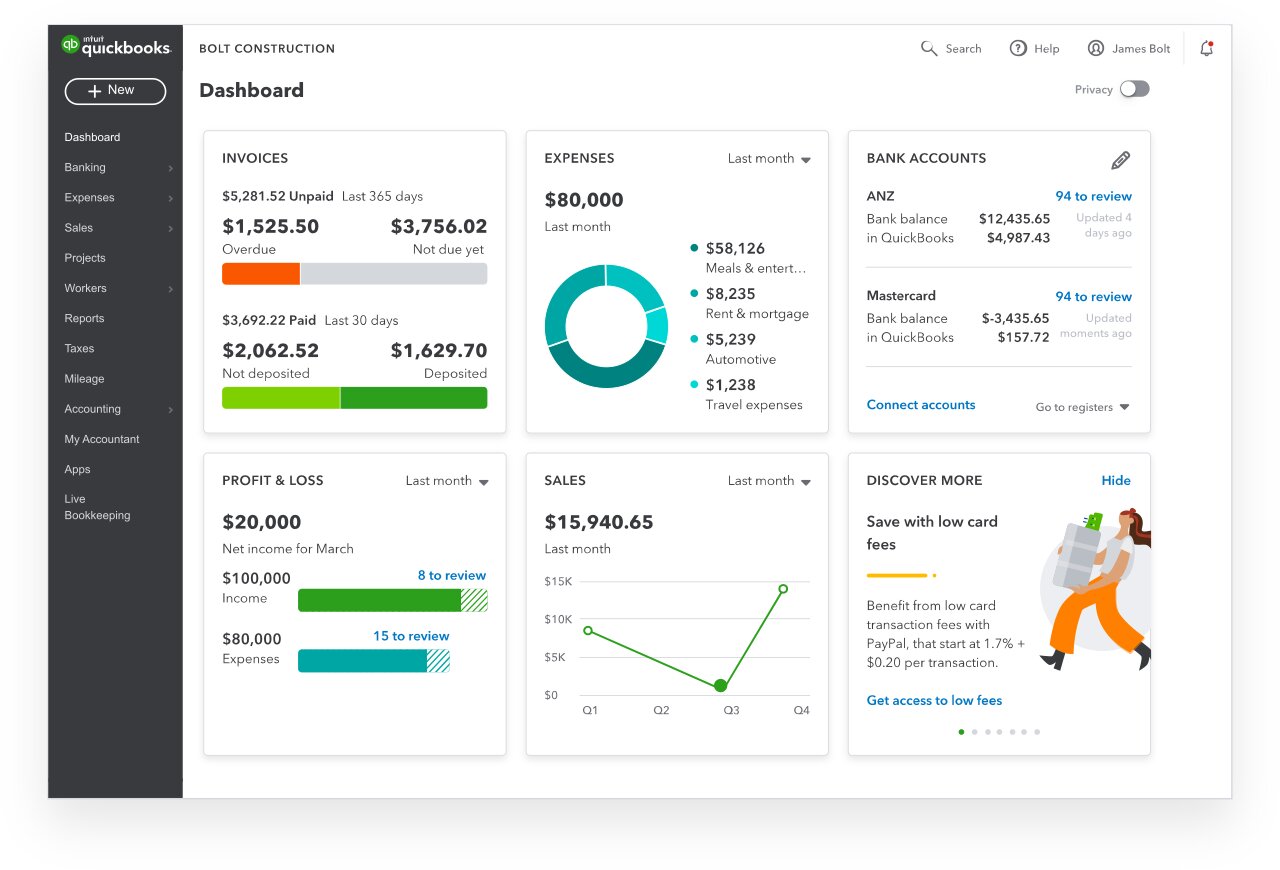

3. QuickBooks Online

Source: QuickBooks Intuit

QuickBooks is one of the most used accounting software in the world. Businesses of all sizes can benefit from this bookkeeping software, but small and medium-sized companies benefit the most. QuickBooks Online (QBO) is cloud-based and integrates with Hostfully and several other PMS.

Key features and benefits

- Classes tracking: QBO lets you assign classes to separate the entries per category. This is particularly useful for categorizing expenses by property.

- Reporting: this software generates downloadable reports for you to share with property owners, co-hosts, or accountants. These include profit & loss, expenses, and balance sheets.

- Schedule payments: depending on the plan you use, you can schedule bill payments and choose which account to pay vendors from.

Pricing

QuickBooks Online has different plans starting at $25 per month. They offer 30% off for the first three months when you sign up for any of their plans.

Pros

- QBO is a well-known software tool with straightforward access to advisers familiar with the software, including CPAs and tax professionals (usually known as QuickBooks Pro Advisors)

- It has a mobile app for tracking your expenses wherever you are.

- Many time-saving apps easily integrate, including several property management software tools, like Hostfully.

- Automatic bank feeds help with the effortless recording of transactions and reconciliation of bank & credit card accounts.

Cons

- According to some users, some customization options for bills, invoices, reports, and charts may be limited.

- It can take some time for users to understand the platform as it has many different functionalities.

- It might be necessary to hire an expert to help you set up your QBO account for short-term rental accounting. Getting the correct settings based on the VRM trust accounting model and your specific business needs requires a certain level of accounting systems expertise.

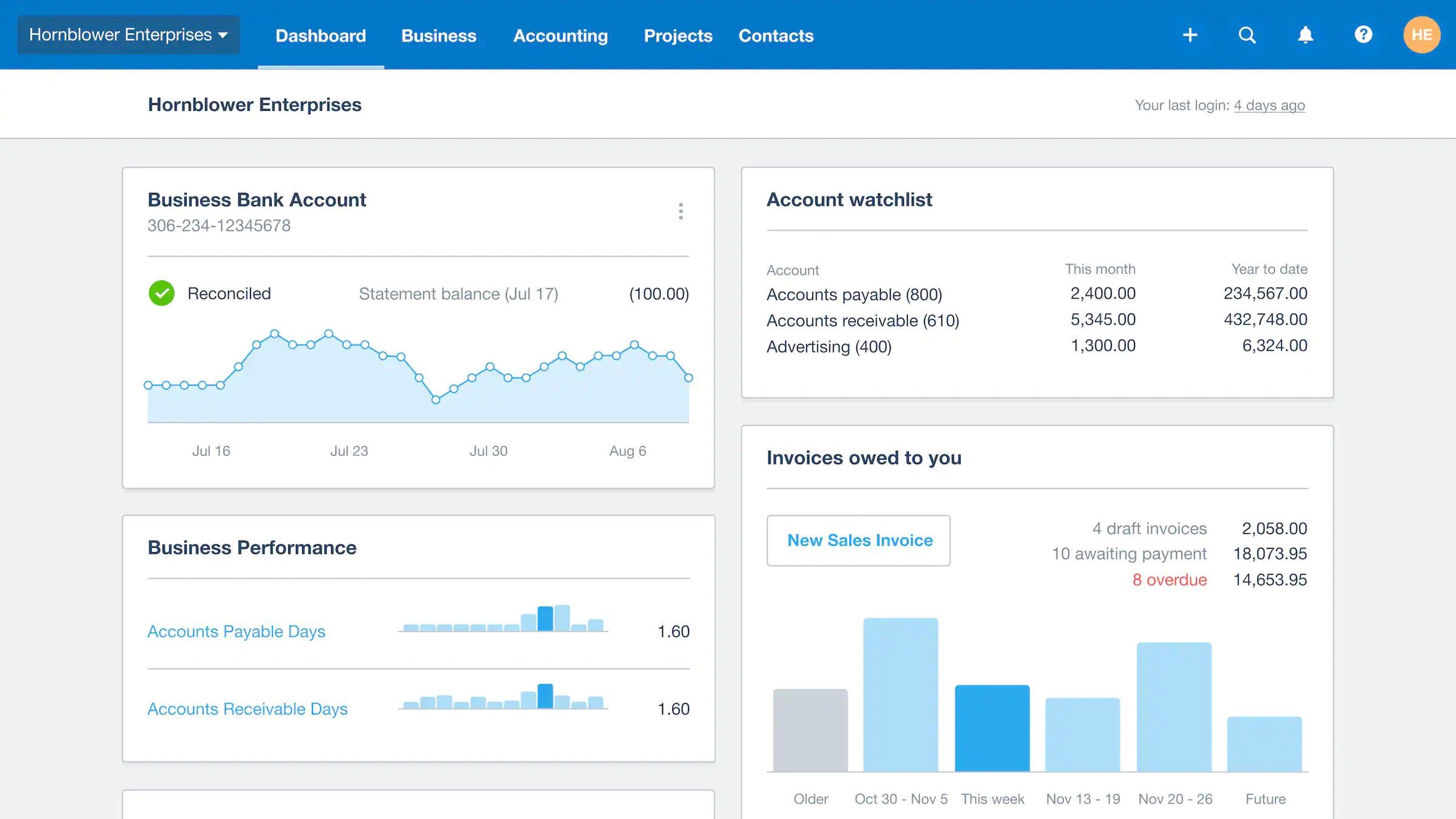

4. Xero

Source: Xero.com

Xero is web-based accounting software for businesses of all sizes. It records entries for bookings, purchases, bills, and other expenses. In addition, you can assign those records to guests, vendors, employees, or items.

Key features and benefits

- Assigning expenses to properties: the ability to assign different entries to a particular property makes it easier to review different rentals.

- One-click reconciliation: at any time of the month, Xero has a button that lets you reconcile all income and expenses and you can see your numbers for the month.

- Interactive profit and loss report: Xero’s profit and loss report lets you click on any of the listed entries to get more info. You can access the invoice attached with just one click. You can also compare the reports against other of your properties or periods.

Pricing

Xero offers different plans that give you access to different features. You can use this software for at least $22 per month.

Pros

- All Xero plans allow for unlimited users.

- It’s user-friendly and easy to use. Plus, it has great customer service.

- Xero offers more robust and accessible custom financial reporting.

- You’ll enjoy easy upload of transactions, which is not a function of QBO except with the use of third-party apps. This is handy when transferring data from VRM booking apps.

Cons

- Like QBO, Xero may require duplicate entries when billing expenses are paid on the owners’ behalf and billing property management fees/commissions.

- Xero offers multi-currency support on its most premium plan. It can be expensive to subscribe just to access this additional feature.

- It integrates with several PMS but doesn’t connect directly to Hostfully. However, you can use Xero and Hostfully together if you’re doing it through Ximplifi.

5. Sage Intacct

Source: SageIntacct.com

Sage Intacct is an advanced financial and accounting software. They promote themselves as suitable for small and mid-sized accounting firms, but due to their advanced features and allegedly high prices, it’s more suited for larger businesses. It’s particularly useful for customers that are finding QBO restraining.

Key features and benefits

- Financial dashboard: Sage Intacct has an interactive dashboard that contains the most relevant financial and accounting information. These dashboards can include different information depending on each target user.

- Consolidate at any time: this software allows you to consolidate your accounting information at any time, so you can always have the most updated information in your financial dashboard. Sage Intacct also supports multiple currencies and consolidates all the information under one for easier analysis.

- Supports different hospitality business models: this tool supports different ownership structures. You can report and review profits for franchises, fractional ownership, global business units, and other shared-revenue models.

Pricing

Sage Intacct doesn’t disclose pricing on its website. However, BT Partners has shared its costs ranged between $15,000 to $60,000 per year.

Pros

- Sage Intacct offers robust multi-entity and multi-ledger financial management solutions. This makes accounting easy for the property manager (PM) and trust accounting for owners.

- It offers several different dimensions (known as classes in QBO) to tag and track transactions. This makes customizing financial reporting, automating owner statements, reporting per booking, and data analysis powerful and easy.

- They offer an open API, which allows for custom integration of VRM apps for streamlined and automated accounting of bookings.

- It allows for template uploads to transfer data easily from the PMS to the back-end accounting system.

Cons

- Sage Intacct requires a more complex setup from one of their partners.

- It’s highly expensive for property owners or managers. It might be more appealing to big property management companies.

- It integrates with several PMS but doesn’t connect with Hostfully. However, just like Xero, you can use this platform through the Ximplifi integration or Open API connection.

6. FreshBooks

Source: Capterra.com

Freshbooks is an accounting software aimed at service-based professionals who charge by the hour. However, it’s a great choice for managing your STR accounting needs. FreshBooks is one of the least expensive options and it’s easy to use.

Key features and benefits

- Mobile app: FreshBooks makes it easier for you to update invoices and add entries on the go. You can use your camera to scan invoices or create them directly from the app. Plus, you can stay on top of notifications and answer comments from your phone.

- Automated expense tracking: this tool connects directly to your bank account and keeps automatic track of all your expenses. You can then update and recategorize these entries if needed.

- Add billable expenses to invoices automatically: FreshBooks lets you mark expenses as billable or not billable and then, see the billable records automatically in your invoices. This feature is particularly useful for co-hosts and small property managers because it lets you invoice the owners for additional business expenses (i.e., restocking broken plates).

Pricing

FreshBooks is one of the most price-effective solutions. Pricing starts at $15 per month and they offer 60% off for the first four months.

Pros

- FreshBooks uses double-entry accounting, which means you’ll always have access to trust-worthy data and calculations of your profit and losses.

- This software offers different categories that simplify tax season. Allowing you to spend less time filling out your tax return.

- FreshBooks has a shallow learning curve. The platform is intuitive and easy to use.

Cons

- FreshBooks isn’t the best choice for people who manage more than one property since it doesn’t allow you to make detailed reports per unit.

- This platform doesn’t allow you to customize your invoices as much as users would want.

- If you’re using WePay to receive payments from your direct booking website or any listing site that uses this J.P. Morgan product, FreshBooks might not be your best choice. Users online complain about the WePay-FreshBooks integration.

- FreshBooks doesn’t support trust accounting.

What to look for in accounting software for vacation rentals

Before you set your mind on one accounting software for your Airbnb or vacation rental, make sure you research if it:

- Integrates with your PMS

- Fits your budget

- Has the features you need

Integrations

To access all your information in one place, your accounting software needs to connect to your PMS, just as your vacation rental channel management tool does.

If you’re using Hostfully as a property management software, you should look into QuickBooks Online. If you want to use Xero or Sage Intacct, you can do it through Ximplifi (and get professional accountants to help you operate the tools).

Pricing

While price is important, if you’re doing trust accounting, you can’t skimp on price. Good accounting software will simplify your taxes and reduce any risk of not complying with local regulations.

The most effective accounting software isn’t the most expensive or cheapest one, it’s the one that fits your bookkeeping, invoicing, and reporting needs.

Functionality

While most accounting software has similar features, some may be a better fit for your requirements. Once you’ve identified your needs, you can match them with each platform’s features. For example, if you’re a hands-on property manager, you probably want to use a tool that lets you upload invoices for supplies and restock expenses on the go.

How do I set up my accounting software?

Since most people choose to use QuickBooks Online, we’ve broken it down for you. There are other ways to set up QBO for trust accounting of property rentals, but this is generally the industry-recommended setup.

1. First steps

- Create your account on QBO.

- Customize your company account and settings. You can edit your company information, billing subscription, sales, expenses, time, and more advanced options.

- Set up your chart of accounts. You’ll need to include an:

- Operating Cash Account for the property manager.

- Escrow Cash Account in the Owners’ books.

- Owner Payment/Draw Account. Note that this account will be set up as an equity account to track payments to owners.

- Connect your business bank accounts, credit cards to use for any STR expenses, and other accounts like PayPal.

- Set up your service inventory so you can easily invoice or pay bills later on. Include as services:

- Compensation (if you’re a co-host or property manager)

- Hosting fees

- Cleaning

- Maintenance

- Taxes

- Insurance

Once you create the services make sure you select the right income account for each one so you can separate expenses by property.

2. Business specifications

To use QBO for your hospitality business, you should create custom fields for each listing or property. Your guests should be set as customers. However, note that this can create issues with short-term rentals if you have repeat renters that rent out multiple homes with multiple owners.

3. Additional customization

Classes

Another way to review your properties is by creating classes. You’ll use classes to track location in the PM books and the owner’s books.

Verify that you allow the tracking “byline” instead of by invoice or bill. This can come in handy if you get statements that have expenses for multiple properties on the same bill. Also, having a “top-class” that represents owners and a “sub-class” for the property locations is very helpful if you manage multiple homes for the same owner.

We recommend turning on the feature in QBO that warns you when a class is not being used as well. This ensures that the owner/property manager always tracks income and expenses.

Billable expenses

Make sure you turn this tracking feature on in QBO. Note that you would only use this feature in the PM books for expenses billable back to the owner.

When the expenses are payable by the owner, they will be paid out of the escrow account in the owners’ books. The expense will just need to be recorded in the correct account and assigned to the appropriate class or tracking category (i.e., property and owner).

Should you use a Vacation Rental Management app?

A vacation rental management app or property management software (PMS) is a crucial piece of tech if you want to scale your short-term rental business. But you don’t need just any PMS: you need one that integrates with your preferred accounting tool.

If you’re planning to use Hostfully as your property management platform, you can pull your QuickBooks Online or Ximplifi data to generate a financial report for owners. This document contains information on:

- Scheduling

- Financial reporting

- Payment distribution

You can also build automations to:

- Send monthly statements

- Adjust for capital expenses

- View owner revenue share

- Distribute payments

Can you just use a VRM app? Or should you also use accounting software?

In general, if you manage fewer than five properties, you can probably get away with only using a VRM app and a spreadsheet. But it isn’t a great idea since it’s easier to make mistakes with manual processes.

Using a PMS like Hostfully helps you automate, standardize, and streamline the following processes, so nothing slips through the cracks.

- Collect payments from bookings

- Pay owners and property managers

- Charge for additional services

- Hold security deposits

- Prepare and share owner’s reports

You should consider one of the tools mentioned above if you need to invoice contractors, pay bills, and calculate taxes. If you want it to integrate with Hostfully, you should pick between QBO or Ximplifi.

One bank account or two?

Some US states guidelines dictate that property management companies need to set up two accounts, but other states don’t have the same requirements. Yet, we believe that you need at least two bank accounts (at least) to properly do trust accounting and simplify bank reconciliation.

One of trust accounting’s law requirements is that there isn’t any commingling of company funds and property owner funds, using separate bank accounts is the best way to achieve that.

The first account is typically an operating account, which holds funds that belong to the PM. The second is an escrow account that holds rental and security deposits, and rental revenues owed to the owners not yet paid out.

Key challenges with vacation rental trust accounting

Trust accounting has some differences from typical business bookkeeping. These can become challenges that you need to be aware of. Some challenges include:

Commingling funds

The very best choice a property manager can make is to keep separate bank accounts for property owner funds (escrow account) and property manager funds. While this can sound more complicated at first, it’s easy to stay on track with accounting software that reconciles payments.

Preserving your ethical responsibilities

The vacation rental manager holds a significant fiduciary responsibility to their vacation rental owners. Do not take this responsibility lightly. Ensure a high level of transparency at the beginning to gain and preserve trust.

Even if you’re a property owner managing your properties, you still need to be ethical in the way you manage your funds. Plus, you can be subject to an audit and you need to have your books in order.

Following state laws and regulations

Every state has its own rules for trust accounting. It’s the property manager‘s responsibility to ensure that everything is being followed appropriately. You can be fined for not following the law.

Vacation rental accounting software: essential to manage your STR

Keeping track of your monthly income and expenses is essential if you manage STR. At first, it’s quite common to do it using a spreadsheet, but as your business grows, you need to pay for accounting software to:

- Support your STR business growth

- Have easy access to insights and make data-driven decisions

- Avoid making manual mistakes

- Start doing trust accounting and:

- Avoid commingling funds

- Be ethical

- Follow local laws and regulations

Before choosing vacation rental accounting software for your business, you should narrow down your options and answer these questions:

- Does it integrate with your PMS?

- Does it fit your budget?

- Does it come with the core functionality that you need?

Pay for the accounting software that gets the most positive responses. If budget is your most important criterion, you should go with FreshBooks. It lacks some analysis functionality but you can start using it for $15 a month.

You should consider QuickBooks Online if you’re looking for a specialized accounting tool that integrates with Hostfully and lets you track expenses for multiple properties. In addition, QBO is one of the most popular accounting software and it will save you a lot of time and money.

If you don’t ever want to make calculations and invoices for your STR business, Ximplifi will simplify your life. This company works with QBO, Xero, or Sage Intacct as accounting software, and gets real accountants to do the work for you for a cheaper price. Ximplifi also connects with Hostfully so you can create accurate and fast owner financial statements.

This is an updated guest post from Jesse King Ehret, Founder and CXO at Ximplifi. If you want to learn more about how technology can simplify your vacation rental accounting, check out their website.

Frequently asked questions about vacation rental accounting software tools

What is accounting software for vacation rental properties?

Accounting software for vacation rental properties is a tool that property managers and owners use to keep track of the income and expenses of their short-term rentals. There is some accounting software that integrates with PMS so owners and managers can see all the information from their rentals in one place.

What is the difference between accounting software and bookkeeping software?

Accounting and bookkeeping software are similar yet different. A bookkeeping software records entries for all income and expenses. It’s basically a data storage tool. Accounting software also has bookkeeping capabilities but includes other accounting features like forecasting, reporting, and cash flow analysis.

How does accounting software help you automate your short-term rental business?

Accounting software is a way of automating your short-term rental business income and expenses data entry. It helps you create automatic invoices for guests and create easier and faster invoices for other service providers. Depending on the software that you choose, you can grant access to your bank account, so the accounting platform can record all accounting transactions automatically.