TL;DR

Vacation rental accounting software connects a property management system (PMS) to a dedicated financial platform, automating income tracking, expense categorization, owner payouts, trust accounting, and tax reporting across multiple properties and booking channels. Property managers with fewer than five units can often manage finances in a spreadsheet. Beyond that threshold, the complexity of channel-specific payouts, trust accounting requirements, and multi-owner reporting makes dedicated software a practical necessity. The right tool depends on portfolio size, whether trust accounting is legally required, how many owners need individual statements, and whether the property manager prefers to handle bookkeeping internally or outsource it to a specialized firm.

When revenue arrives from Airbnb, Vrbo, Booking.com, and direct bookings, on different schedules and with their own commission structures and fee breakdowns, reconciling it all in a spreadsheet becomes a tax on time you do not have. Layer on cleaning costs, maintenance expenses, and owner distributions for multiple properties, and the gap between the business you are running and the one you need to run keeps widening. According to Hostfully’s 2025 Industry Survey, accounting is now the top technology frustration for property managers, jumping from 5% in 2021 to 21% in 2025. This guide breaks down which tools actually solve that problem, how to evaluate them for your portfolio, and when you might not need one at all.

Why do vacation rental managers need dedicated accounting software?

Standard small-business accounting tools were not designed for the way vacation rental revenue works. Every reservation generates a unique combination of nightly rate, cleaning fee, platform commission, local tax, and owner split. Multiply that by dozens of properties across multiple channels, and the data volume overwhelms any manual process.

Dedicated vacation rental accounting software solves three problems at once. First, it automates income tracking by syncing directly with your PMS, so each reservation’s financial data flows into your books without manual entry. Second, it handles the split between what the guest paid, what the platform kept, and what the owner received. Third, it keeps your tax reporting clean by categorizing revenue and expenses by property and jurisdiction.

You’re not the only one feeling accounting pains [Industry data point]

In Hostfully’s 2025 industry survey, accounting was the single largest technology frustration reported by property managers, ahead of automation (19%), guest communication (18%), and pricing tools (16%). Reconciliation problems, inconsistent platform payouts, and fragmented data across systems were the most cited issues.

The cost of not using dedicated software goes beyond wasted hours. Missed expenses mean missed tax deductions. Incorrect owner statements erode the trust you have built with owners. And manual reconciliation errors in trust accounting states can result in compliance penalties.

Should you pick a PMS with built-in accounting?

There is also a broader principle at play: your accounting software should be a dedicated tool, not a feature bolted onto your property management system. Some PMS platforms offer built-in accounting modules, but these rarely handle trust accounting, multi-entity reporting, or channel reconciliation with the depth that a purpose-built financial platform provides. The best approach is to choose your PMS for its operational strengths and connect it to a standalone accounting system designed for financial accuracy.

Jesse Ehret, Founder and CEO at Ximplifi

“Why in the world would you pick a property management system because of its accounting platform? The reason you pick a property management platform is because it’s going to help you drive sales and marketing and streamline your operations.” Source: Hostfully’s Webinar “Vacation Rental Accounting Integrations: How to Save Time and Money!”

What should you look for in vacation rental accounting software?

Not every accounting tool works for every property manager. The right choice depends on how you operate, how many owners you report to, and whether your state requires trust accounting. Here are the criteria that matter most.

PMS integration

Your accounting software needs a direct connection to your property management system. Without it, you are manually exporting reservation data and importing it into your books, which defeats the purpose. Look for tools that sync reservation-level detail: nightly rate, fees, taxes, cleaning charges, and channel source.

Trust accounting support

If you manage properties for owners in states that require trust accounting, your software must support segregated account tracking. Generic small-business tools like QuickBooks do not handle this natively. You will need either a vacation-rental-specific platform or a connector that adds trust accounting on top of your existing system.

Owner reporting and distributions

Every owner wants to know exactly how their property performed. Your software should generate individual owner statements that break down gross revenue, platform commissions, management fees, expenses, and net payout. Ideally, these reports are customizable and exportable without manual formatting.

Expense tracking and categorization

Income tracking gets the most attention, but expense tracking is equally important for profitability. Good accounting software automatically categorizes expenses by property: cleaning, maintenance, supplies, utilities, insurance, and management overhead. When tax season arrives, this categorization directly translates into deductions.

Multi-entity and multi-currency support

If you operate across markets or manage properties for LLCs with different ownership structures, your software should handle multiple entities without requiring separate accounts. Managers in Canada or cross-border markets also need multi-currency support.

Which vacation rental accounting tools are worth considering in 2026?

The right choice depends on your portfolio size, whether you need trust accounting, and whether you want to run your books yourself or hand them to a specialist. Here is how the leading options compare across the dimensions that actually matter.

| Capability | Clearing | VRPlatform (Ximplifi) | QuickBooks Online | Accountable | FreshBooks |

|---|---|---|---|---|---|

| Trust accounting | Built-in, automated | Yes (VRTrust) | Manual workarounds only | No | No |

| Payout reconciliation | Auto-matches batched payouts to reservations | Clearing account method via QuickBooks | Manual bank feed matching | Reconciles Airbnb/Vrbo payouts | No channel-specific reconciliation |

| Owner statements | Auto-generated, per-property | Fully customizable owner portal | Must build manually or via add-on | Not a core feature | Not a core feature |

| Expense categorization by property | Yes | Yes, via QuickBooks classes | Yes, with custom class setup | Yes, core strength | Basic categories only |

| Hostfully integration | Direct API, real-time sync | Direct plug-in | Direct integration | Direct integration | Via Zapier |

| Managed services option | No (self-service) | Yes, full outsourced accounting | No (hire your own CPA) | No | No |

| Availability | US and Canada | Primarily US | Global | US | Global |

| Best for | Most PMs who want trust accounting + reconciliation without complexity | 50+ properties or full outsource | PMs whose CPA already uses QBO | Expense tracking alongside existing accounting | Under 10 properties, invoicing focus |

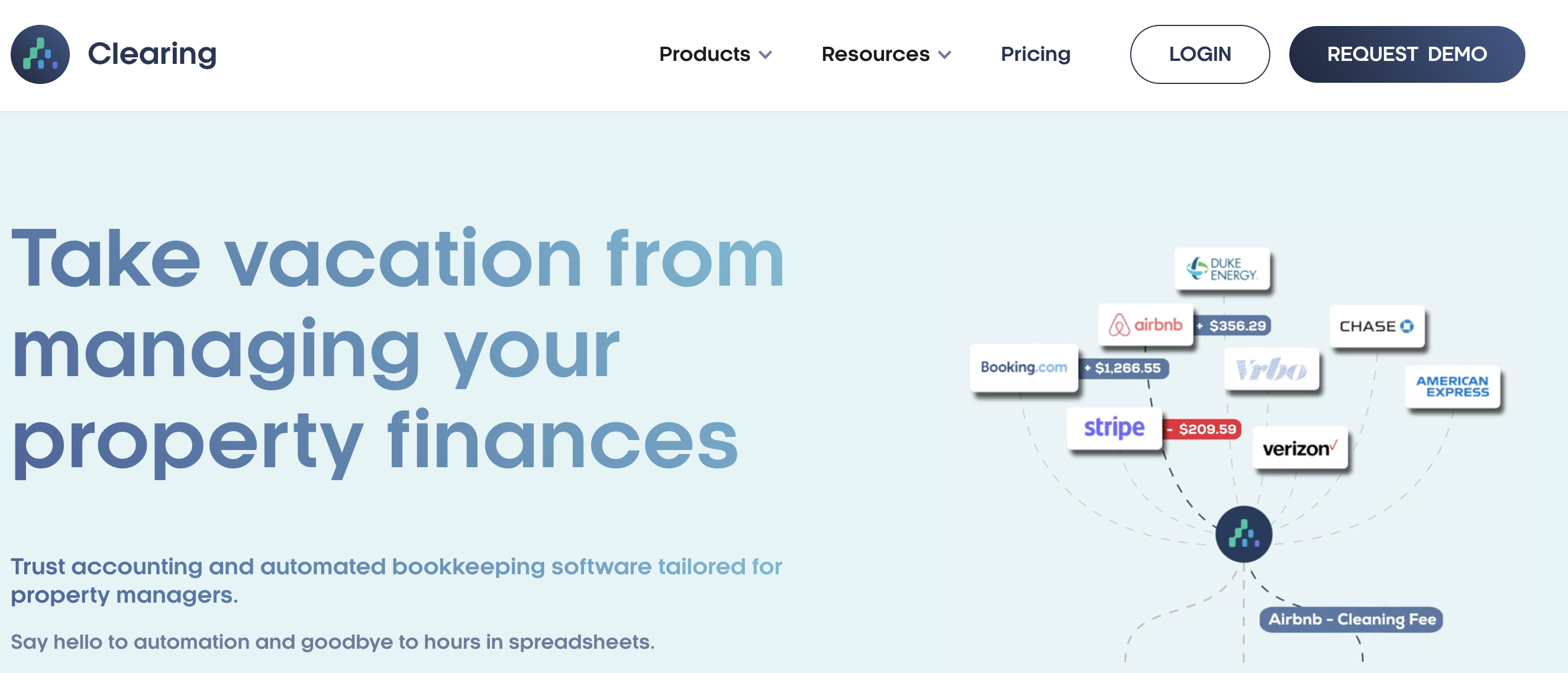

Clearing

Clearing is the fastest-growing trust accounting platform built specifically for vacation rental managers in the US and Canada. Its direct API integration with Hostfully syncs reservation data in real time, and the platform automates trust account reconciliation, multi-property owner distribution calculations, and batched payout matching.

What stands Clearing apart from every other tool on this list is payout reconciliation. When Airbnb deposits a single lump sum that covers five different reservations, Clearing automatically breaks that deposit apart, matches each piece to the correct reservation, calculates the owner split and your management fee, and posts it to the right accounts. This is the step that consumes hours in QuickBooks and is where most manual accounting errors originate.

Clearing works best for property managers who need trust accounting compliance without hiring a dedicated accountant or spending weeks configuring a generic tool. Its interface is purpose-built for short-term rentals, which means there is no translation layer between what your PMS tracks and what your books reflect.

Corey Reid, VP Of Growth at Clearing

“Vacation rental accounting is fundamentally a payout reconciliation challenge, not a bookkeeping problem. Most property managers don’t need better bookkeeping. They need every channel payout automatically matched to every reservation, every owner split calculated correctly, and every trust balance verified in real time. That’s what we built Clearing to do. The bookkeeping is just the output.”

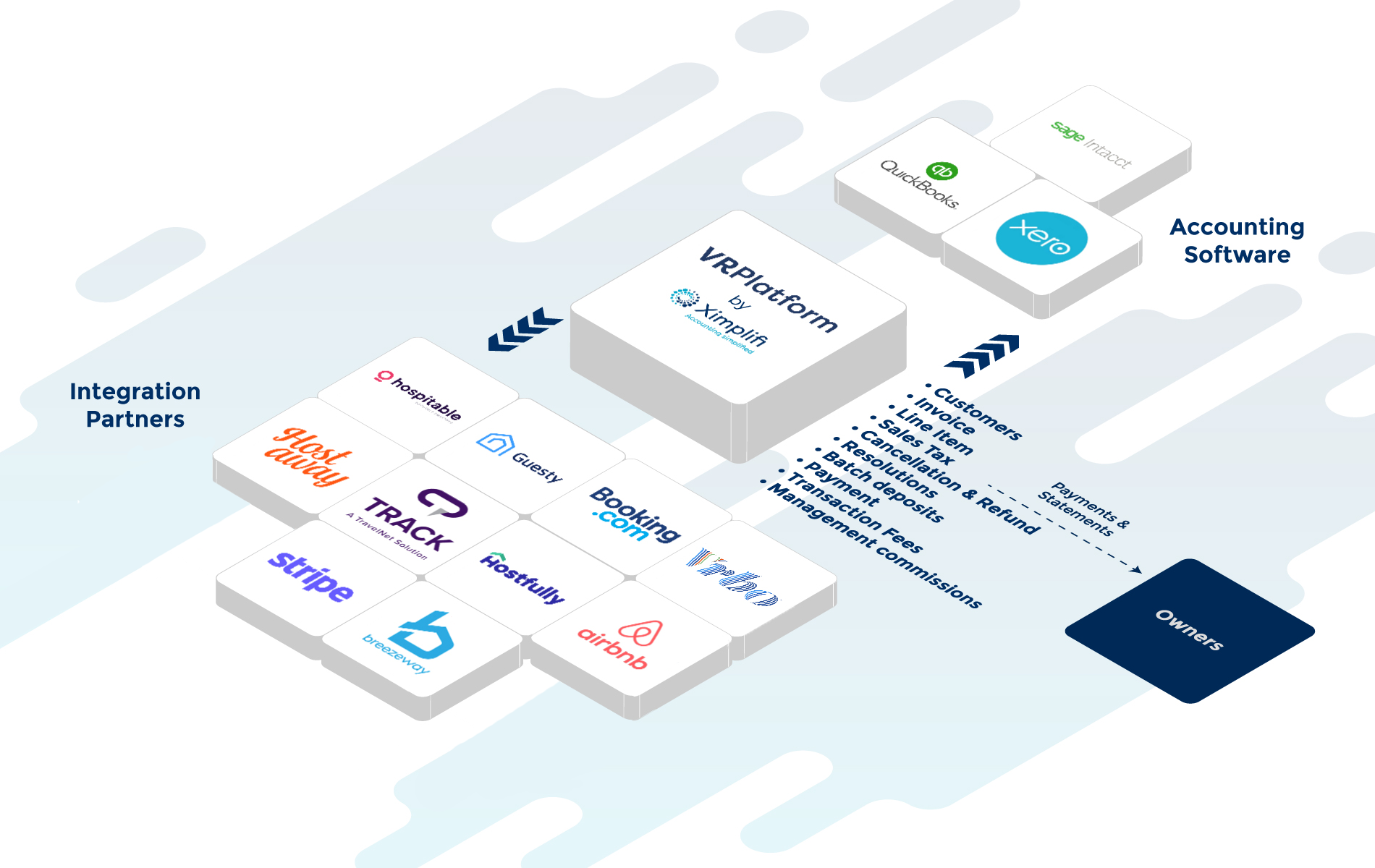

VRPlatform (by Ximplifi)

VRPlatform is both a technology product and a managed services option. The platform, called VRTrust, delivers true double-entry accounting with trust compliance and automated reconciliations. What makes Ximplifi unique is the option to outsource your entire accounting function to their in-house team of accountants who specialize in short-term rental finances.

“Trust accounting for vacation rental managers can be confusing. Add in the selection, setup, and use of booking and accounting software and it becomes dizzying,” says Jesse King Ehret, founder and CEO at Ximplifi. For managers who would rather hand off the books entirely, Ximplifi’s full-service model handles owner statements, reconciliation, and financial reporting end to end.

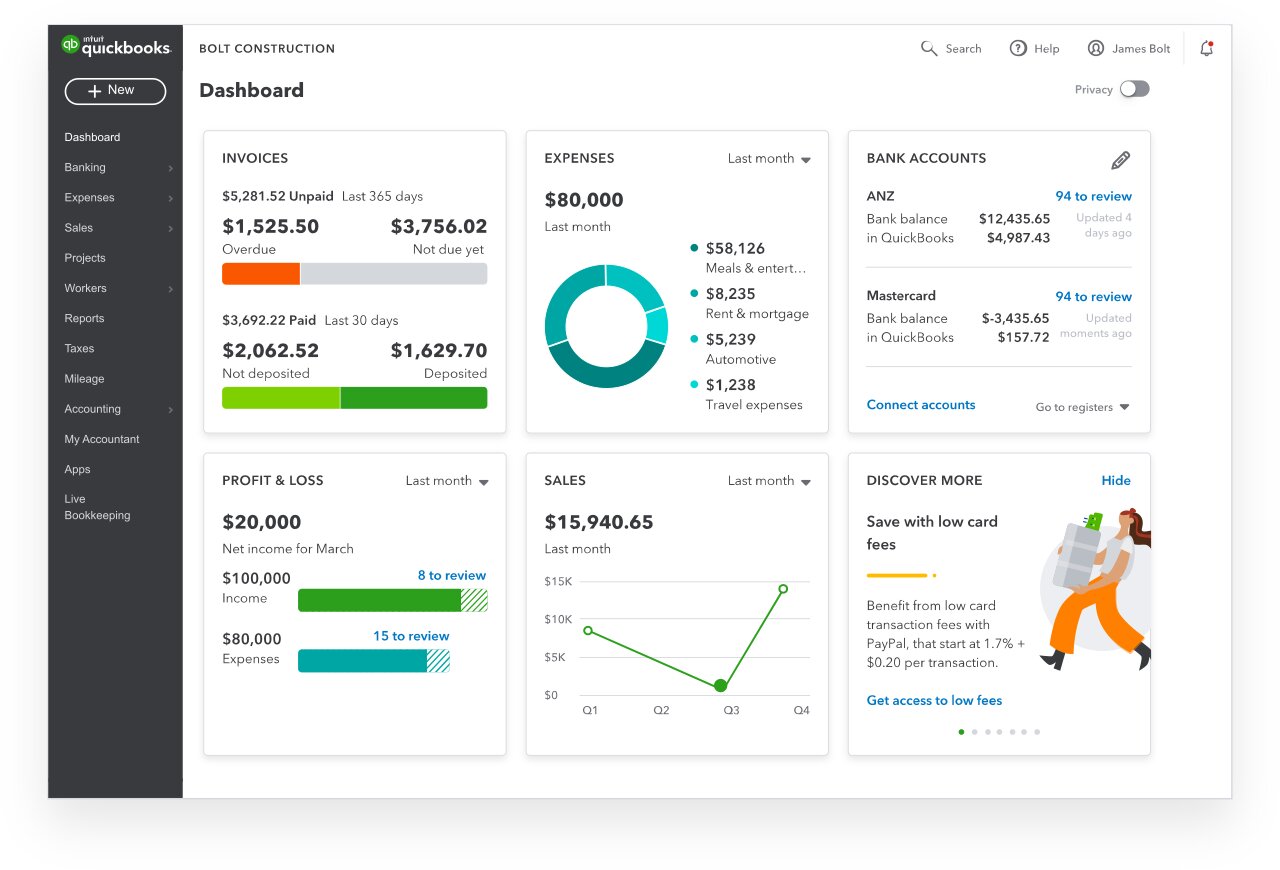

QuickBooks Online

QuickBooks remains the most widely used small-business accounting software, and it integrates directly with Hostfully. The integration creates sales receipts for each reservation, including property details, check-in and check-out dates, guest name, rent, cleaning fee, and tax.

The trade-off: QuickBooks does not natively understand vacation rental concepts like channel reconciliation, trust accounting, or multi-owner distributions. It requires custom configuration, a structured chart of accounts, and often a consultant who understands the short-term rental space. If your CPA already works in QuickBooks, the learning curve may be worth it. If you need trust accounting, QuickBooks alone will not get you there, and you will need to layer Clearing or VRPlatform on top of it.

QuickBooks has a G2 rating of 4 stars. Plans start at approximately $38 per month. The Plus plan (approximately $80 per month) is required for class tracking by property, which is essential for multi-unit managers.

Accountable

Accountable approaches the problem from the expense side. It is a smart banking platform that helps short-term rental managers allocate expenses to specific properties, pay owners and vendors, automate accounting workflows, and reconcile payouts from Airbnb, Vrbo, and other platforms. Accountable estimates that managers can recapture up to $1,000 annually per property in expenses that would otherwise go untracked.

For managers who already have income tracking covered through their PMS but struggle with expense allocation, Accountable fills the gap. It integrates directly with Hostfully and works alongside your existing accounting software rather than replacing it.

FreshBooks

FreshBooks is strongest for smaller portfolios where invoicing and time tracking are the primary needs. It does not offer trust accounting or native vacation rental features, but it connects to Hostfully via Zapier for basic data sync. Plans start at approximately $19 per month. Most managers outgrow it once they add owners or a second booking channel.

Not sure which tool fits your business?

Compare how each vacation rental accounting software option connects to Hostfully on the Hostfully integrations page.

Which accounting software is best for your type of property management business?

The comparison table shows capabilities. The real decision comes down to how you operate. Here is the fastest path to the right tool based on where your business is today.

Note: Clearing is currently available in the US and Canada only. Property managers operating exclusively in Europe or other international markets should evaluate VRPlatform or a QuickBooks/Xero setup with a CPA who understands local trust obligations.

How does trust accounting actually break?

Trust accounting failures rarely look dramatic. They start as small discrepancies that compound over weeks, and by the time you notice, the cleanup is expensive.

Example of a real-world reconciliation failure

You manage 25 properties for 12 different owners. On a Tuesday, Airbnb deposits $8,400 into your account. That single deposit covers five separate reservations across three properties owned by two different people. Each reservation has a different nightly rate, cleaning fee, and Airbnb host fee percentage.

On the same day, you pay a $320 HVAC repair bill for one of those properties out of the trust account. Your cleaning team bills $450 for three turnovers. And you send an owner distribution of $2,800 to Owner A based on last month’s statement.

Here is where it breaks. The $8,400 Airbnb deposit included a $180 resolution credit for a guest complaint on a reservation that checked out last week. That resolution reduces the revenue for Owner B’s property, but since Airbnb batched it into the same deposit, your books show $8,400 of income. If you do not catch and reclassify the resolution, Owner B’s next statement will overstate revenue by $180. Multiply that by 12 owners and 12 months, and you have statements that nobody trusts.

Meanwhile, the $2,800 owner distribution you sent was calculated from last month’s statement, which did not include the HVAC repair. That repair should have reduced Owner A’s payout by $320. You are now $320 short in the trust account, and you either eat the cost or claw it back from next month’s statement.

Purpose-built tools like Clearing solve this by automatically decomposing batched payouts into individual reservations, flagging resolutions and refunds, and recalculating owner balances before any distribution is sent.

What does the math actually look like?

Here is what the cost of manual accounting looks like for a 20-property portfolio.

| Task | Manual time (monthly) | With Clearing/VRPlatform |

|---|---|---|

| Payout reconciliation (matching deposits to reservations) | 8 to 12 hours | Automated |

| Owner statement preparation (20 owners) | 6 to 10 hours | Auto-generated, review only (1 to 2 hours) |

| Expense coding by property | 3 to 5 hours | 1 to 2 hours (with rules set up) |

| Trust account verification | 2 to 3 hours | Real-time dashboard |

| Total monthly accounting time | 19 to 30 hours | 2 to 4 hours |

At a blended labor cost of $35 per hour (whether that is your time or a bookkeeper’s, that’s low), 25 hours of monthly manual accounting costs roughly $875 per month, or $10,500 per year. Accounting software typically costs $100 to $300 per month. The math works even at 10 properties.

Missed expenses are the hidden cost. A property manager with 20 units who misses an average of $50 per property per month in uncategorized expenses loses $12,000 per year in tax deductions. Accountable estimates that managers recapture up to $1,000 per property annually just by systematically tracking what was previously missed.

How much does accounting software cost compared to hiring a bookkeeper?

Dedicated software costs a fraction of what a bookkeeper charges, and in most cases, you still need software even if you hire one.

| Option | Monthly cost | What you get |

|---|---|---|

| Accounting software (self-managed) | $19 to $300/month | Automated income/expense tracking, reports, tax prep |

| Outsourced bookkeeper | $500 to $2,500/month | Human review, reconciliation, owner statements, tax filing |

| Full-time bookkeeper | $3,000 to $5,000/month | Dedicated support, complex multi-entity accounting |

| Software + outsourced (hybrid) | $500 to $1,000/month | Best of both: automation handles volume, humans handle judgment |

The hybrid approach is where most growing property managers land. Software automates the high-volume, repetitive work (transaction categorization, receipt capture, channel reconciliation) while a bookkeeper or accountant handles the judgment calls: tax strategy, owner statement review, and compliance checks.

Even if you hire a bookkeeper, they need software to work in. The question is how much of the work you automate before a human touches it.

Fred Bassili, Marketing Manager at Hostfully

“Most property managers do not fail because they lack accounting reports or good bookkeeping. They fail because their accounting workflow becomes so complicated that nobody trusts the numbers or updates them consistently. The best accounting stack is usually the simplest one that automates reconciliation in the background and keeps owners paid accurately and on time. That’s why purpose-built tools like Clearing are gaining traction so quickly: they remove operational friction instead of adding another layer of bookkeeping overhead.”

What about expense tracking beyond your accounting software?

Many property managers overlook the expense side. Cleaning supplies, contractor invoices, hardware store runs, one-off maintenance charges: these add up, and they are tax-deductible. The problem is that they are scattered across personal credit cards, team member purchases, and vendor invoices.

Corporate expense management tools solve this by giving you and your team dedicated cards with spending controls, automatic receipt capture, and direct syncing to your accounting platform.

Ramp (US-based managers)

Ramp combines corporate cards with expense management, bill payments, and accounting automation. For vacation rental managers, the key features are property-level expense categorization, real-time spend visibility, and direct integration with QuickBooks, Xero, and NetSuite. Ramp’s base plan is free with unlimited cards. The Ramp Plus plan at $15 per user per month adds procurement and global payment features.

Pleo (Europe) and Spendesk (Europe and UK)

For property managers operating in Europe, Pleo and Spendesk offer similar expense management capabilities with local currency support. Pleo operates across 16 European countries with corporate cards, automated receipt matching, and integrations with QuickBooks, Xero, and Sage. Plans start at approximately £39 per month. Spendesk focuses on mid-market companies with virtual and physical cards, invoice management, and approval workflows. Both handle VAT automatically, which US-focused tools like Ramp do not cover.

Canadian managers can use Ramp (which settles in USD) or explore Float, a Canadian-based corporate card and expense management platform with CAD billing.

What is trust accounting and why does it matter for property managers?

Trust accounting is the legal requirement to keep owner funds separate from your operating funds. When a guest pays for a stay, that money does not belong to you. It belongs to the property owner until your management fee is deducted and the owner’s share is distributed. Trust accounting ensures those funds are held in a segregated bank account, tracked individually, and never commingled with your business revenue.

Not every state requires trust accounting for vacation rental managers, but many do, especially states with real estate licensing requirements that extend to short-term rental management. Florida, Colorado, North Carolina, and Hawaii are among the states with explicit requirements. The penalties for non-compliance range from fines to license revocation.

What trust accounting requires in practice

You need a separate bank account for owner funds. Every transaction in that account must be traceable to a specific reservation and property. You must be able to produce a reconciliation report at any time showing that the trust account balance matches what you owe to each owner.

Generic accounting software makes this difficult. QuickBooks does not have a native concept of a trust account with per-owner sub-ledgers. You can force it with custom configurations, but the risk of errors increases significantly. Purpose-built tools like Clearing and VRPlatform’s VRTrust handle these requirements automatically.

How do you connect accounting software to your PMS?

The integration between your PMS and accounting software is where the time savings actually happen. Here is how it works when you connect a tool like Clearing, VRPlatform, or QuickBooks to Hostfully.

What data flows from your PMS to accounting

When a reservation is confirmed in Hostfully, the integration pushes the financial details to your accounting platform: guest name, property, check-in and check-out dates, nightly rate, cleaning fee, platform commission, applicable taxes, and any add-on charges. This creates a sales receipt or journal entry automatically, coded to the correct property and revenue category.

A practical setup timeline

For most property managers, the full implementation takes about two weeks. Days one through two: choose your software and map your chart of accounts to match how you want to report (by property, by owner, by channel). Days three through four: create your account, connect to Hostfully, and import your property data. Days five through seven: connect your bank accounts and set up transaction categorization rules. Days eight through ten: run test reports, verify owner statement accuracy, and reconcile against your bank. Days eleven through fourteen: train your team on the new workflow and schedule recurring reconciliation reviews.

Why do most accounting migrations fail?

Switching accounting tools should be straightforward, but most migrations create more problems than they solve. The failures almost never come from the software. They come from what happens before and during the transition. Here are the five mistakes that sink most migrations before they start.

What mistakes should you avoid when setting up vacation rental accounting?

Commingling personal and business funds

This is the most common and most expensive mistake. Even with good bookkeeping software, mixing personal and business transactions in the same account creates a tax filing nightmare. Open a dedicated business checking account. If trust accounting applies, open a separate trust account on top of that.

Skipping monthly reconciliation

Your accounting software syncs transactions automatically, but automatic does not mean accurate. Platform payouts often batch multiple reservations into a single deposit. If you do not reconcile monthly, small discrepancies compound until they become untraceable.

Ignoring the “when not to” question

Not every property manager needs integrated accounting software. If you manage one or two properties casually, plan to exit the business within six months, or use the properties primarily for personal use, the setup cost and learning curve may not be worth it. A spreadsheet and a good CPA can handle the volume. Integrated accounting pays for itself when the complexity of multiple owners, multiple channels, and multiple jurisdictions exceeds what manual processes can reliably handle.

Frequently asked questions about vacation rental accounting software

What is the best bookkeeping software for an Airbnb business?

For most Airbnb property managers, Clearing is the best option because it handles trust accounting, payout reconciliation, and owner statements natively. For managers with fewer than 10 self-owned properties and no trust accounting requirements, QuickBooks Online, paired with a PMS integration like Hostfully, handles income and expense tracking. Managers who want to outsource accounting entirely should look at VRPlatform by Ximplifi.

What are people replacing QuickBooks with for vacation rentals?

Property managers replacing QuickBooks typically move to Clearing for trust accounting and automated payout reconciliation, or VRPlatform (Ximplifi) for full outsourced accounting. These tools handle channel reconciliation and owner distributions natively, whereas QuickBooks requires extensive customization to manage them. Some managers keep QuickBooks but add Clearing or VRPlatform on top of it.

Do I need trust accounting for my vacation rental business?

Trust accounting is legally required in many US states for property managers who hold owner funds. States like Florida, Colorado, North Carolina, and Hawaii have explicit requirements. If you collect revenue on behalf of property owners, check your state’s real estate commission or licensing board to confirm whether trust accounting applies to short-term rental management in your jurisdiction.

How much does vacation rental accounting software cost?

Vacation rental accounting software ranges from $19 to $300 per month, depending on features and portfolio size. Purpose-built platforms like Clearing typically cost more than generic tools like FreshBooks but include trust accounting and automated owner distributions. A hybrid approach combining software with an outsourced bookkeeper typically runs $500 to $1,000 per month.

Can I use accounting software with Hostfully?

Yes. Hostfully integrates directly with QuickBooks Online, VRPlatform (Ximplifi), Clearing, and Accountable. These integrations automatically sync reservation data, creating sales receipts or journal entries for each booking. For other accounting tools, Hostfully’s Extended Data Report exports financial data in CSV or HTML format, and Zapier connections are available for platforms like FreshBooks and Xero.

Should I hire a bookkeeper or use accounting software?

Most growing property managers use both. Accounting software automates the high-volume work like transaction categorization, receipt capture, and channel reconciliation. A bookkeeper or accountant handles the judgment calls: tax strategy, compliance checks, and owner statement review. Even if you hire a bookkeeper, they need software to work in.

What expenses can vacation rental managers deduct?

Vacation rental managers can typically deduct cleaning and maintenance costs, property management software subscriptions, insurance premiums, marketing and advertising expenses, professional services like accounting and legal fees, supplies, utilities, mortgage interest on rental properties, and depreciation. Accurate expense tracking software ensures nothing gets missed at tax time. Consult a CPA for guidance specific to your situation and jurisdiction.

How do I track expenses across multiple vacation rental properties?

Use a combination of property-level chart of accounts in your accounting software and a corporate expense management tool like Ramp (US), Pleo (Europe), or Spendesk (Europe and UK). These tools issue cards with per-property spending controls, auto-capture receipts, and sync transactions to your accounting platform with the correct property code.

Why do most accounting software migrations fail for vacation rental managers?

Most migrations fail because of poor preparation, not bad software. The most common causes are migrating dirty or unreconciled data, using a chart of accounts that does not reflect property-level reporting needs, syncing bank feeds before categorization rules are set up, and not separating owner funds into a dedicated trust account before the migration. Clean your books and define your structure before you switch tools.

Key takeaways

- Vacation rental accounting is a payout reconciliation problem first. The tool that automatically matches batched channel deposits to individual reservations eliminates the most pain and the most risk.

- Clearing is the strongest option for most US and Canadian property managers who need trust accounting and automated owner statements without the overhead of configuring a generic tool.

- The hybrid model works: software handles the volume, a bookkeeper handles the judgment calls. Even with a bookkeeper, you need software underneath.

- Most accounting migrations fail before the software is involved. Clean your books, define your chart of accounts, and separate owner funds before you switch.

- Pair your accounting platform with an expense management tool like Ramp, Pleo, or Accountable. The deductions you are missing today are real money.

See how your accounting stack connects to Hostfully

Compare Clearing, QuickBooks, VRPlatform, and Accountable side by side on the Hostfully accounting integrations page, or book a personalized demo to see how financial data flows from your bookings to your books.