Renting out your property short-term is a great way to make extra income, but it also means you need to change how you think about insurance. Once guests arrive, your home shifts from a private residence to a business — even if you only host occasionally.

The main thing to know is that standard homeowners insurance isn’t designed for short-term rentals. Without the right cover, you could face serious problems if a guest causes damage or gets injured.

Getting insurance right from the start can help you avoid costly surprises. So, let’s unpack what short-term home insurance covers, how much it costs, the options available, and how to choose the right protection.

What is short-term home insurance?

Short-term rental insurance is designed to cover the risks of renting out a property for temporary periods. This includes reservations made through platforms like Airbnb and Vrbo, as well as direct reservations made through your own website or system.

Policies typically protect you from financial loss resulting from:

- Damage to your property

- Liability if a guest or third party gets injured

- Legal costs

- Loss of income

- Theft and vandalism

This type of insurance is intended to work for a range of hosts. Primary homeowners renting out a spare room during peak season might choose a policy that only activates for a few weeks at a time. On the other hand, property managers are more likely to look for continuous coverage.

Why homeowner’s insurance doesn’t cover your business

Homeowner’s insurance doesn’t cover short-term rental activities quite simply because they’re not intended for commercial use. Once you start accepting paying guests, your risk profile changes.

Because of this, many standard policies explicitly exclude short-term rental activity. Insurers won’t cover you for any property damage or injuries that happened on the premises once they see you’re operating as a business. Even minor incidents, such as a broken appliance or a short hospital trip for a sprained ankle, can result in a denied claim.

Many areas also make proper insurance a legal requirement. For example, short-term rentals in the District of Columbia must secure at least $500,000 in liability insurance.

Misty Valdez, owner of 282 Timbuktu Cabin, says short-term rental insurance should become a serious concern before you ever host your first guest. “Once I decided to use my cabins as short-term rentals, I knew a standard homeowners policy wasn’t going to be enough,” she says “Having paying guests come and go changes everything, especially when it comes to liability.”

How much does short-term home insurance cost?

Recent Airbtics data shows that short-term home insurance can range from $80 to $300 per month. The exact cost depends on factors, such as your:

- Property type

- Location

- Average occupancy levels

- Appliances and amenities

- Proximity to water

For example, a villa with a swimming pool that you rent all year-round is likely to have a high monthly premium. A rural home that only accepts guests for a few weeks each year will be substantially lower.

The same Airbtics report suggests it’s best to think of insurance in terms of ROI rather than costs. Although you may end up spending $2,400 per year on coverage, you’re shielding your business from a potential loss of almost $100,000.

What are the options for short-term home insurance?

There are three types of short-term home insurance with a clear winner:

Platform-provided protection

Many booking platforms include some form of host protection that applies automatically when a reservation is made through their system. Airbnb’s Aircover is one of the most well-known examples.

At first, it might seem like there’s a simple choice between free Aircover and paid insurance. The problem is that platform coverage is often limited and doesn’t cover many types of property damage or liability. For example, this unlucky host found that Aircover wouldn’t pay his claim after a fire that led to his entire $1 million property burning down.

Rami Sneineh, owner of Insurance Navy Brokers, says it’s best not to rely on platform protection. “New entrants usually risk their whole investment on such guarantees,” he says, “According to my experience in the business, this cover is not actual insurance and hardly ever covers liability of the guest or theft.”

Extension or endorsement to an existing policy

Some insurers let you add an extension or endorsement to your existing homeowner’s policy to cover short-term rental activity. These add-ons are often cheaper than specialist policies and can work well if you only host occasionally.

The trade-off is that there’s often narrower coverage and stricter limits. If you plan to scale and expand your business, this option is likely to be too restrictive.

Specialist short-term rental insurance

Specialist short-term rental insurance is a custom policy. Because they’re designed for your business operations, they leave fewer gaps in your coverage and give you more flexibility over packages.

Especially if you own a luxury property or manage multi-unit rentals, specialist short-term rental insurance is the only option. It can prevent you from losing a significant portion of your earnings and business assets to a legal claim.

What short-term home insurance does and doesn’t cover

Before arranging vacation rental insurance, it’s important to understand what it usually covers. You may still need to plug some gaps with additional policies.

| Does cover | Doesn’t cover |

|

|

Top short-term home insurers compared

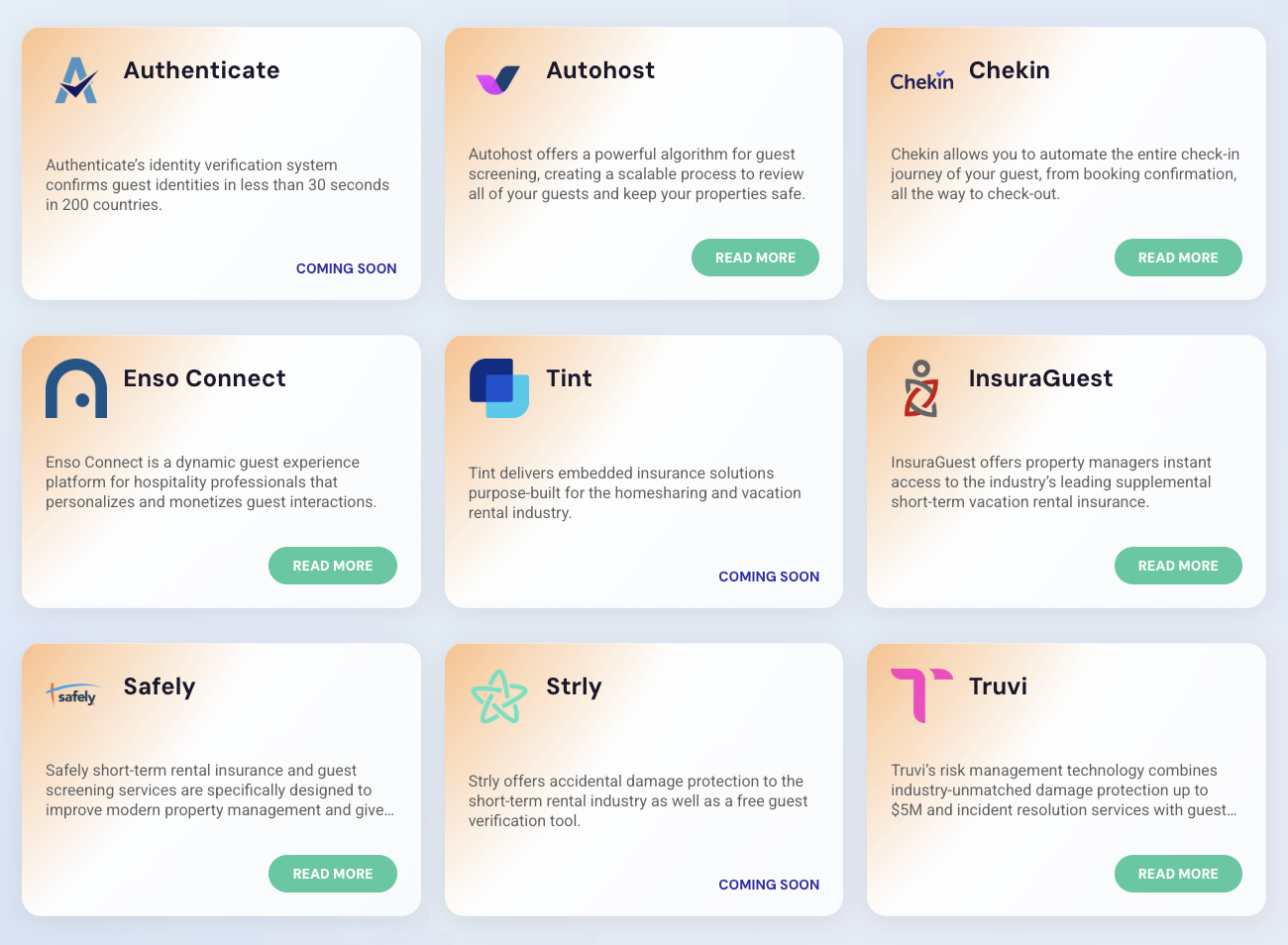

Knowing which insurance providers to trust to provide you with full coverage can be challenging. Hostfully has vetted and partnered with some of the leading solutions on the market to make finding coverage simpler.

Here’s a quick breakdown of their key selling points:

- InsuraGuest: Complements your existing homeowner’s policy with up to $25,000 in medical coverage no matter who’s at fault.

- Safely: Combines guest screening with high-limit damage and liability protection.

- Strly: Customizable policies with payouts within 72 hours of reported guest damages.

- Tint: Specialized coverage for vacation rentals with flexible limits and durations.

- Truvi: Automated guest screening plus damage protection for up to $5,000,000.

By choosing insurers through Hostfully’s integration marketplace, policies will come into effect automatically. You can continue to manage these from a single centralized dashboard instead of juggling multiple platforms.

How to choose the right short-term home insurance for your risk profile

Hosts might be tempted to choose the option that appears cheapest. However, this is a false economy when the savings you make can quickly turn into massive losses when a guest makes a significant legal claim.

Before committing to a policy, step back and consider the following factors to make sure your policy matches your risk profile:

- Property type: Apartments, single-family homes, and luxury properties all carry different levels of risk. Your property generally has a higher risk profile if it has multiple levels, outdoor areas, or balconies.

- Location: Your location can affect the types of risk to your vacation home. For example, coastal regions are often more prone to severe weather phenomena that can cause wind damage and flooding.

- Occupancy levels: Hosting guests all-year round increases the chances of something going wrong so aim for comprehensive coverage. If you only accept guests for a few nights a year, flexible or per-night coverage may be enough.

- Local regulations: Some jurisdictions require a minimum amount of insurance before they allow you to get licensed. Check that local providers can provide this level of coverage.

- Ability to scale coverage: If you plan to add more listings or increase occupancy, prioritize finding an insurer that lets you easily increase limits. Scalable coverage helps you avoid switching providers as your hosting operation expands.

Common short-term home insurance mistakes to avoid

Even hosts who understand the basics of short-term rental insurance can make costly mistakes. These issues often come from assumptions, convenience, or trying to save money in the short-term.

Here are the pitfalls to avoid to make sure you have the right insurance in place from the start:

Assuming all regions work the same way

Most states and countries have their own rules for insurance. Germán Ceballos, owner of Uppsala House, recommends that hosts do their own research before they start comparing providers.

“When I started, I assumed I’d need specialized STR insurance like you’d get in the US,” he says “Turns out, in Sweden, many standard home insurance policies already include coverage for short-term rentals as part of their package! I just had to confirm with my provider that hosting was covered, and I was set.”

Choosing the cheapest policy

Price matters, but the cheapest policy isn’t always the best fit. Lower monthly premiums often come with reduced limits, narrower coverage, or exclusions that only become clear when you file a claim.

Instead of focusing on the price, compare what the insurer covers and how they handle claims. If you accept guests all-year round, you’ll eventually have to deal with a guest injury or some property damage. Always prepare for the worst-case scenario when arranging insurance.

Overrelying on insurance

Aim to reduce risk and prevent things from going wrong as well as insuring your business. Although providers can cover some financial losses, they can’t protect you from a bad reputation if guests frequently suffer injuries or losses at your vacation home. For example, frequent falls on a slippery bathroom floor can quickly turn into a slew of negative reviews and a poor rating.

Sneineh points out that reducing risk can also lower insurance costs. “Controlled security devices and smart locks should also be installed so that your risk profile can be reduced,” he says “These upgrades in my situation save you a good percentage on your yearly premiums.”

Treating insurance as separate from ongoing operations

Insurance shouldn’t be something you set up once and forget. As your portfolio grows and you accept more guests, your risk exposure changes too.

Review your coverage at least once a year and whenever your setup shifts. For example, you should check your policies whenever you:

- Add a property

- Expand into a new location

- Install new amenities

- Change your pricing

- Hire more staff

By continuously reviewing your policies, you avoid gaps in protection and may even find opportunities to adjust limits or reduce costs.

Waiting until a claim to get your documentation in order

Many hosts only think about the paperwork once something goes wrong. But if something goes wrong, insurers may deny your claim if you don’t have proof of what actually happened.

Keep clear records as part of normal operations. You should aim to save everything from booking details and guest messages to before and after photos of properties during turnover. If you use a PMS like Hostfully, you can keep much of this information organized in one place, so you’re not scrambling to piece it together later.

Find the perfect partner to protect your STR with Hostfully

Short-term home insurance isn’t just a box to tick. It’s a core part of running a business that requires a deep understanding of the risks of your specific setup. Policies must always match how you actually operate, from the type of guests you host to your house rules and your communication style.

But insurance works best when it is integrated into your day-to-day operations rather than handled separately. That is where Hostfully PMS comes in with:

- Short-term rental insurers through our Integration Marketplace

- Automated insurance activation alongside bookings

- Security deposits with full control over terms and amounts

- Data syncs across channels to avoid risky double bookings

- Guest screening and ID verification with integrated partners

- Centralized guest communication to track messages and help resolve claims

When your insurance works well with your system, you reduce risk, simplify management, and create a long-term strategy for growth.

FAQs about short-term home rental insurance

Does homeowners’ insurance cover Airbnb rentals?

No, standard homeowners insurance usually doesn’t cover short-term rentals. Most policies exclude any type of business activity, including hosting guests. You typically need a specialist policy or an approved endorsement to ensure there are no gaps in your coverage.

Do I need insurance if I only rent a few times per year?

Yes, even occasional hosting carries business risk because a single accident or damage claim can be costly. Some insurers offer policies that activate only during booked stays.

Will my homeowners’ policy be cancelled if I start hosting on Airbnb?

Yes, it can be if you don’t disclose the activity. Insurers may deny claims, refuse renewal, or even cancel policies with immediate effect if you don’t arrange proper coverage. Always contact your insurance provider when you switch from homeownership to commercial use or make significant changes to your business operations.